*This post may have affiliate links, which means I may receive commissions if you choose to purchase through links I provide (at no extra cost to you). As an Amazon Associate I earn from qualifying purchases. Please read my disclaimer for additional details. Thank you for supporting the work I put into this site!

Sinking funds are something should be included in everybody’s budget in some capacity. A sinking fund is money set aside to cover a future expense.

This can be a fixed expense or a variable expense. Some people may just have a handful of sinking funds, others may have quite a few. Each person is different. Let’s work through some basics.

Sinking Funds Definitions & Considerations

What is a Sinking Fund?

A sinking fund is a way to budget for items you don’t necessarily purchase each month but want to be sure to budget for so you have the money when the time comes to pay for something or spend from that category.

Want vs Need

Sinking fund items can be classified as wants or needs:

Want = This is a charge that isn’t guaranteed to happen or that you could do without if you absolutely had to. If you have a true emergency come up (i.e. job loss, major medical, etc) these items could be completely eliminated.

Need = No matter what, you are going to have to pay for this. These are items you can’t go without.

When is the item due?

If you are just starting to set up your sinking funds, your expenses may be higher now but will get lower as time goes on. If you need money by a specific date, you need to take that into account when determining the amount to budget each month for that sinking fund category. For example:

Today is April 21st. I have one more paycheck on April 30th. I want to start saving for my car insurance which is due every six months, and next due in June at $124. There are two ways to budget for this in my sinking funds:

- Will I have money to pay for it on my next paycheck? If so I can take the total amount / 3 = $42 . I would budget $42 for April, May and June.

- If I don’t have the money to pay for it this month then I need to take the total amount / 2 = $62. I would budget $62 for May and June.

Regardless of which way I currently have to budget, $42 or $64, Starting in July the budget amount goes down to $21 per month. That’s because this bill is due every six months and $124 / 6 = $21 (I always round up)

Cap

For items with a specific amount, a cap doesn’t apply. The cap is the amount that will be due. For items with variable or undetermined amounts, it is best to set a cap.

This is the maximum amount of money you want to save in this category. It can be high or low and it is OK for some categories to have no cap i.e. down payment savings.

For other categories it makes more sense to budget with a cap (i.e. Christmas savings).

Amount Due per Month

The amount due per month is the amount you want to put into that sinking fund category each month. There are three possible ways to calculate this value:

- Amount Due / # months till Due Date = Amount to Budget Per Month

- i.e. Amt Due = $125

- # months left until the bill is due = (5)

- Amount to budget per month = $25

- Sinking Fund Cap / # months you think is reasonable = Amount to Budget Per Month

- i.e. Down Payment fund might be a 5-year goal at $30k.

- $30k / 5 years = $6k / year

- $6k / 12 months = $500 per month to be saved in sinking funds

- Dollars you are willing to contribute to that sinking fund each month.

- Lets say you want to save for a new couch that is $800 and you think you can afford $20 per month. Put the $20 into your sinking funds. Save more when you can but otherwise, the fund will be at $800 when it reaches $800.

Possible Sinking Funds Categories

Here are some ideas:

- Amazon Prime

- Back 2 School

- Books

- Car Insurance

- Car Repairs

- Christmas

- College Fund

- Crafting

- Decor

- Domain Registration

- Emergency Fund

- Fully Funded Emergency Fund (FFEF)

- Gifts

- Health Insurance (co-pays, medicine, etc)

- HOA Fees

- Home Maintenance

- Domain Hosting

- House Down Payment

- Legal

- Liability Insurance

- Life Insurance (annual)

- New Car

- Propane

- Property Taxes

- Vacation

- Vehicle Registration

Planning Out Your Sinking Funds

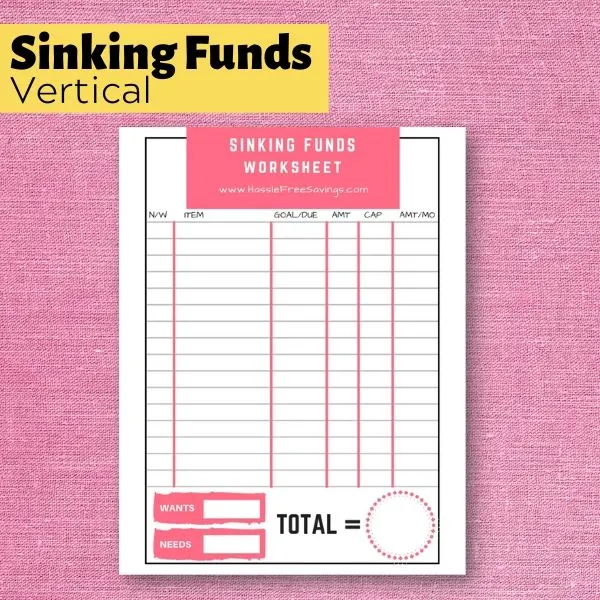

The first year you decide to start using sinking funds things are going to be a little bit different. If you are like most people, you just floated each bill as it came up.

That means when your $500 car insurance renewal hit in June, you only worried about it in June. With sinking funds, you’ll be budgeting a little bit each month so that when the time comes, you already have enough saved for that bill and don’t even have to worry about it.

To help with that, I developed this worksheet in a vertical format with printable instructions. It is available for FREE in the resource library when yous signup for the newsletter.

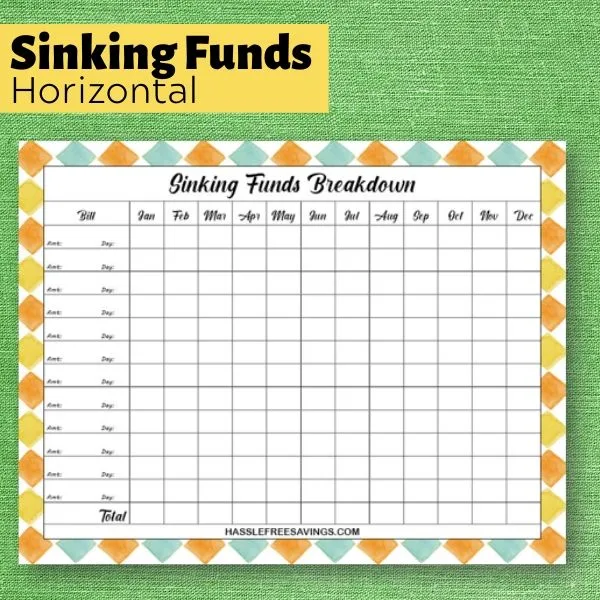

Getting Caught Up With Sinking Funds

The first year you set up your budget, your sinking funds amounts aren’t going to always be straight forward.

Depending on when you start, and when each bill is due, the amount you pay each month will vary until you get caught up.

If it is February, and you have a bill due once a year in June, what you save in your sinking funds that first March, April, and May will be different than what you need to save on a routine basis.

This second free sinking fund printable is to help you plan out your sinking funds for the first 12 months of your budget. After that, your sinking fund amounts should be stable. It is also available for FREE in the resource library.

I am currently (Feb 21) editing a video that will walk you step by step through using both spreadsheets so you can start implementing them into your March budget!

Lisa

Saturday 29th of February 2020

Thank you for all your help! You are Amazing!